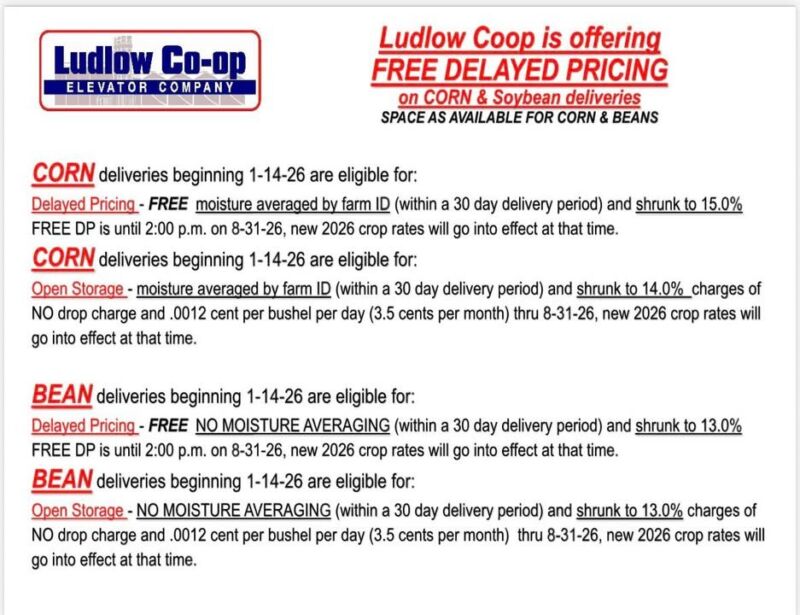

CORN deliveries beginning 1-14-26 are eligible for:

Delayed Pricing –FREE moisture averaged by farm ID (within a 30 day delivery period) and shrunk to 15.0% FREE DP is until 2:00 p.m. on 8-31-26, new 2026 crop rates will go into effect at that time.

CORN deliveries beginning 1-14-26 are eligible for:

Open Storage – moisture averaged by farm ID (within a 30 day delivery period) and shrunk to 14.0% charges of NO drop charge and .0012 cent per bushel per day (3.5 cents per month) thru 8-31-26, new 2026 crop rates will go into effect at that time.

BEAN deliveries beginning 1-14-26 are eligible for:

Delayed Pricing –FREE NO MOISTURE AVERAGING (within a 30 day delivery period) and shrunk to 13.0% FREE DP is until 2:00 p.m. on 8-31-26, new 2026 crop rates will go into effect at that time.

BEAN deliveries beginning 1-14-26 are eligible for:

Open Storage – NO MOISTURE AVERAGING (within a 30 day delivery period) and shrunk to 13.0% charges of NO drop charge and .0012 cent per bushel per day (3.5 cents per month) thru 8-31-26, new 2026 crop rates will go into effect at that time.

This is the list of the newly elected board members who will be serving for the 2025/2026 fiscal year.

Roger Gustafson (Paxton) – President

Kenny During (Rantoul)– Vice President

Robert Schmid (Buckley)– Secretary

Cory Roelfs (Rantoul)– Treasurer

Steve Glazik (Paxton)

Dan Kief (Loda)

Jeff McGehee (Onarga)

Brent Neukomm (Cissna Park)

Jim Niewold (Loda)

Mike Otto (Buckley)

Pat Quinlan (Ludlow)

2025 Annual Meeting of the Stockholders will be held:

Wednesday, September 03, 2025

The Cadillac 108 W State St. Paxton, IL

Doors open at 6:00 p.m. for registration,

Buffet style dinner from 6:00 p.m. until 7:00 p.m. (Provided by Luke’s one stop)

Shareholders meeting will begin at 7:00 p.m.

🌽 Corn Market Update Corn futures scored new highs for the move on Friday amid what was a slow news day to wrap up February. Market themes are little changed today from what they've been the rest of the week this week, with the coming US growing season and the weather going it gaining almost daily in importance. Sources in South America say current moisture levels throughout a lot of the safrinha area are likely sufficient enough at this point to prevent a disaster, but how good yields end up being is still likely a product of when rains shut off later in the season. The last 20% of the crop is usually at risk of rains shutting off in April/May, and this year appears that it will be no different.

🌱 Soybean Market Update The soy complex was mixed to end the week this week, with the beans higher and the products mixed as traders continue to digest the RVO headlines from earlier this week and debate the likelihood that additional Chinese buying shows up in the short term. Amid the Trump-Xi meeting that is now just a month away seemingly showing signs of falling apart earlier this week, we find the strength in the bean market impressive even if we're not sure how valid it is. If China doesn't buy and weekly inspections take a seasonal dive from here, ending stocks likely increase and would say the market is overpriced. If China buys the full 8 MMTs that Trump is asking for, ending stocks likely decrease, and we would imagine futures test the waters above $12 at some point over the course of the year. Like we've said for several Fridays in a row, its this situation and how it plays out through summer that aside from US weather, has the biggest impact on longer term price direction.

🌾 Wheat Market Update Wheat futures ripped to new highs again on Friday, though we continue to have little good reason as to why amid supply and demand fundamentals that are anything but positive. We've cited technical trading as reason for the prolonged move for days now, but simply have been unable to pinpoint any other factor that would even remotely justify the 70+ cent rally seen since the lows made in January. Once the funds get back to a more neutral position in wheat like they've done in corn recently, it will be interesting to see whether upward momentum continues or if the rally stalls and corrects again into spring. The rally has made US wheat even less competitive on the global market, and has gotten to a point where companies appear to be looking at importing supplies from outside the US and this also adds to what most feel should be a bearish undertone in the space. ... See MoreSee Less

🌽 Corn Market Update May corn futures scored new highs for the move on Thursday, continuing what has been a slow but steady uptrend since the low made shortly following the January WASDE report. News has remained slow, but the market has been well-supported by basis throughout most of the country that has held steady amid what continues to be a strong export program and a farmer that is undersold. Otherwise, longer term price considerations remain a product of US planted acreage and crop sizes in Brazil and Argentina, and we don't see a lot aside from weather in the short term that's going to have much of a material impact on any of these fronts.

🌱 Soybean Market Update Soybean futures, and the overall complex in general, had another bumpy ride on Thursday, with values quite a bit higher into the pause this morning, then quite a bit lower at mid-morning, then near unchanged by the time things were all said and done this afternoon. Like we mentioned at the top, the sheer number of headlines popping up on a near-daily basis has made trading somewhat difficult of late, but the market has still continued to trek higher nonetheless. Contracts from July on took out their fall highs from last year overnight last night, and this tells us that at least for now, the market sees at the very least a non-zero chance that China buys more than the 12 MMTs that would've been priced in last November. This, mixed with what most assume will be increasing demand from the biofuel sector, is at the heart of the rally in beans that has been going on since the beginning of the year. Should the market find out this isn't the case at some point, the 25+ cent plunge today over the span of an hour will likely seem like small potatoes compared to what would likely ensue following such a development.

🌾 Wheat Market Update Chicago wheat futures ended their losing streak at three on Thursday, closing higher for the first day this week on profit taking and global cash tenders that offered support to futures. Given the current discount on Argy wheat compared to the US, weekly export sales data this morning could've been worse, which also likely lent some support to the space throughout the morning and into the afternoon. Otherwise and like the corn market, it was another mostly slow news day here, with there little new in terms of developments on the fundamental front that would have a material impact on futures prices. ... See MoreSee Less

🌽 Corn Market Update Corn futures scored new highs for the move on Friday amid what was a slow news day to wrap up February. Market themes are little changed today from what they've been the rest of the week this week, with the coming US growing season and the weather going it gaining almost daily in importance. Sources in South America say current moisture levels throughout a lot of the safrinha area are likely sufficient enough at this point to prevent a disaster, but how good yields end up being is still likely a product of when rains shut off later in the season. The last 20% of the crop is usually at risk of rains shutting off in April/May, and this year appears that it will be no different.

🌱 Soybean Market Update The soy complex was mixed to end the week this week, with the beans higher and the products mixed as traders continue to digest the RVO headlines from earlier this week and debate the likelihood that additional Chinese buying shows up in the short term. Amid the Trump-Xi meeting that is now just a month away seemingly showing signs of falling apart earlier this week, we find the strength in the bean market impressive even if we're not sure how valid it is. If China doesn't buy and weekly inspections take a seasonal dive from here, ending stocks likely increase and would say the market is overpriced. If China buys the full 8 MMTs that Trump is asking for, ending stocks likely decrease, and we would imagine futures test the waters above $12 at some point over the course of the year. Like we've said for several Fridays in a row, its this situation and how it plays out through summer that aside from US weather, has the biggest impact on longer term price direction.

🌾 Wheat Market Update Wheat futures ripped to new highs again on Friday, though we continue to have little good reason as to why amid supply and demand fundamentals that are anything but positive. We've cited technical trading as reason for the prolonged move for days now, but simply have been unable to pinpoint any other factor that would even remotely justify the 70+ cent rally seen since the lows made in January. Once the funds get back to a more neutral position in wheat like they've done in corn recently, it will be interesting to see whether upward momentum continues or if the rally stalls and corrects again into spring. The rally has made US wheat even less competitive on the global market, and has gotten to a point where companies appear to be looking at importing supplies from outside the US and this also adds to what most feel should be a bearish undertone in the space. ... See MoreSee Less

🌽 Corn Market Update May corn futures scored new highs for the move on Thursday, continuing what has been a slow but steady uptrend since the low made shortly following the January WASDE report. News has remained slow, but the market has been well-supported by basis throughout most of the country that has held steady amid what continues to be a strong export program and a farmer that is undersold. Otherwise, longer term price considerations remain a product of US planted acreage and crop sizes in Brazil and Argentina, and we don't see a lot aside from weather in the short term that's going to have much of a material impact on any of these fronts.

🌱 Soybean Market Update Soybean futures, and the overall complex in general, had another bumpy ride on Thursday, with values quite a bit higher into the pause this morning, then quite a bit lower at mid-morning, then near unchanged by the time things were all said and done this afternoon. Like we mentioned at the top, the sheer number of headlines popping up on a near-daily basis has made trading somewhat difficult of late, but the market has still continued to trek higher nonetheless. Contracts from July on took out their fall highs from last year overnight last night, and this tells us that at least for now, the market sees at the very least a non-zero chance that China buys more than the 12 MMTs that would've been priced in last November. This, mixed with what most assume will be increasing demand from the biofuel sector, is at the heart of the rally in beans that has been going on since the beginning of the year. Should the market find out this isn't the case at some point, the 25+ cent plunge today over the span of an hour will likely seem like small potatoes compared to what would likely ensue following such a development.

🌾 Wheat Market Update Chicago wheat futures ended their losing streak at three on Thursday, closing higher for the first day this week on profit taking and global cash tenders that offered support to futures. Given the current discount on Argy wheat compared to the US, weekly export sales data this morning could've been worse, which also likely lent some support to the space throughout the morning and into the afternoon. Otherwise and like the corn market, it was another mostly slow news day here, with there little new in terms of developments on the fundamental front that would have a material impact on futures prices. ... See MoreSee Less

0 CommentsComment on Facebook